Are cryptocurrencies rising?

You may have noticed that cryptocurrencies have become more popular in the past year. If you compare the popularity that cryptocurrencies are getting today and it received in the past years, you will surely see how this industry has grown.

When the cryptocurrency Exio Coin starts a round of fundraising on Sept. 7, its founders say the unit will come with a unique distinction: the first to be endorsed by a sovereign nation.

The identity of the government backer won’t be revealed until October, and Bloomberg News has no way of verifying the claim of support. According to co-founder Sunny Johnson though, the supporter is one of “the world’s richest countries” on a per capita basis.

The claim of official approval highlights how the boom in cryptocurrencies and their underlying technology is becoming too big for central banks, long the guardian of official money, to ignore. From speculative betting to trading solar power, digital money is proliferating.

Until recently, officials at major central banks were happy to watch as pioneers in the field progressed by trial and error, safe in the knowledge that it was dwarfed by roughly $5 trillioncirculating daily in conventional currency markets. But now as officials turn an eye toward the increasingly pervasive technology, the risk is that they’re reacting too late to both the pitfalls and the opportunities presented by digital coinage.

“Central banks cannot afford to treat cyber currencies as toys to play with in a sand box,” said Andrew Sheng, chief adviser to the China Banking Regulatory Commission and Distinguished Fellow of the Asia Global Institute, University of Hong Kong. “It is time to realize that they are the real barbarians at the gate.”

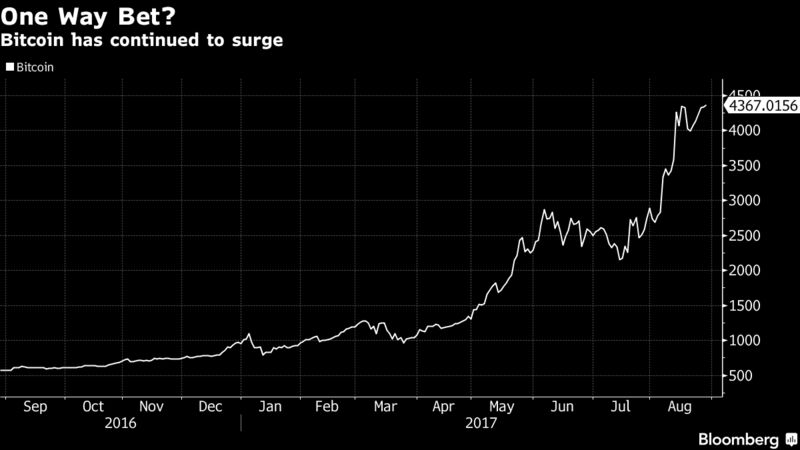

Bitcoin — the largest and best-known digital currency — and its peers pose a threat to the established money system by effectively circumventing it. Money as we know it depends on the authority of the state for credibility, with central banks typically managing its price and/or quantity. Cryptocurrencies skirt all that and instead rely on their supposedly unhackable technology to guarantee value.

China’s Lead

If they don’t get a handle on bitcoin and their ilk, and more people adopt them, central banks could see an erosion of their control over the money supply. The solution may be in the old adage, if you can’t beat them, join them.

The People’s Bank of China has done trial runs of its prototype cryptocurrency, taking it a step closer to being the first major central bank to issue digital money. The Bank of Japan and the European Central Bank have launched a joint research project which studies the possible use of distributed ledger — the technology that underpins cryptocurrencies — for market infrastructure.

The Dutch central bank has created its own cryptocurrency — for internal circulation only — to better understand how it works. And Ben Bernanke, the former chairman of the Federal Reserve who has said digital currencies show “long term promise,” will be the keynote speaker at a blockchain and banking conference in October hosted by Ripple, the startup behind the fourth largest digital currency.

Russia, too, has shown interest in ethereum, the second-largest digital currency, with the central bank deploying a blockchainpilot program.

In the U.S., both banks and regulators are studying distributed ledger technology and Fed officials have made a couple of formal speeches on the topic in the past 12 months, but have voiced reservations about digital currencies themselves.

Policy Issues

Fed Governor Jerome Powell said in March there were “significant policy issues” concerning them that needed further study, including vulnerability to cyber-attack, privacy and counterfeiting. He also cautioned that a central bank digital currency could stifle innovations to improve the existing payments system.

At the same time, central bankers are obviously wary of the risks posed by alternative currencies — including financial instability and fraud. One example: The Tokyo-based Mt. Gox exchange collapsed spectacularly in 2014 after disclosing that it lost hundreds of millions of dollars worth of bitcoin.

But for all their theoretical tinkering, official-money guardians have largely stood by as digital currencies have taken off. The explosion in initial coin offerings, or ICOs, is evidence. Investors have poured hundreds of millions of dollars into the digital currency market this year alone.

The dollar value of the 20 biggest cryptocurrencies is around $150 billion, according to data from Coinmarketcap.com. Bitcoin itself has soared more than 380 percent this year and hit a record — but it’s also prone to wild swings, like a 50 percent slump at the end of 2013.

“At a global level, there is an urgent need for regulatory clarity given the growth of the market,” said Daniel Heller, Visiting Fellow at the Peterson Institute for International Economics and previously head of financial stability at the Swiss National Bank.

Self Interest

Rather than trying to regulate the world of virtual currencies, central banks are mainly warning of risks and attempting to garner some advantage from distributed-ledger technology for their own purposes, like upgrading payments systems.

Carl-Ludwig Thiele, a board member of Germany’s Bundesbank, has described bitcoin as a “niche phenomenon” but blockchain as far more interesting, if it can be adapted for central-bank use. In July, Austria’s Ewald Nowotny said the he’s open to new technologies but doesn’t believe that will lead to a new currency, and that dealing in bitcoin is effectively “gambling.”

There could also be a monetary policy aspect to consider. ECB Governing Council member Jan Smets said in December that a central-bank digital currency could give policy makers more leeway when interest rates are negative. Policy makers have long been concerned that if they cut rates too low, people will simply hoard cash. The ECB’s deposit rate is currently minus 0.4 percent.

Other central banks see the uses of distributed ledger technology, but worry about the abuses virtual money can be put to outside the official system — like criminal money laundering and the sale of illegal goods. That’s not to mention the risk that virtual currencies could pose to the rest of the financial system if the bubble were to pop.

‘Great Promise’

Bank of England Governor Mark Carney — who has said blockchain shows “great promise” — also warned regulators this year to keep on top of developments in financial technology if they want to avoid a 2008-style crisis.

While Mt. Gox cast a shadow over bitcoin in Japan, it now has many supporters in the world’s third-biggest economy. Parliament passed a law in April this year making it a legal method of payment. Japan’s largest banks have invested in bitcoin exchanges and small-cap stocks linked to the cryptocurrency or its underlying technology have rallied this year as it begins to win favor with some retailers.

With the nation’s Financial Services Agency responsible for bitcoin’s regulation, the BOJ remains focused on studying its distributed ledger technology.

Not Ready Yet

“Central banks are not yet ready for regulating digital currencies,” said Xiao Geng, a professor of finance and public policy at the University of Hong Kong. “But they have to in the future since unregulated digital currencies are prone to crime and Ponzi-type speculation.”

To be sure, the attraction of virtual currencies for many remains speculation, rather than for households or companies buying and selling goods.

“It is a fad that will die down and it will be used by less than 1 percent of consumers and accepted by even fewer merchants,” said Sumit Agarwal of Georgetown University, who was previously a senior financial economist at the Federal Reserve Bank of Chicago. “Even if we can make the digital currency safe it has many hurdles.”

The founders of Exio Coin argue they have developed a middle way with principles of governance that will set the trend for the blockchain industry. While some regulation is inevitable, cryptocurrencies are intended to be a global form of currency and not subject to the rules and regulations of one jurisdiction, said Johnson.

With all the misgivings about cryptocurrencies, having a sovereign endorser — rather than an issuer — may be a pragmatic way of offering the benefits of digital money with less of the worry.

“With no one central bank maintaining control Exio Coin will retain its decentralized characteristics,” Johnson said. “The sovereign endorser shares our vision for the future.”

via Bloomberg